There is light at the end of the tunnel for commercial airlines.

As many countries are now reporting declines in the number of new COVID-19 cases, the demand for air travel remains tepid, but increasing. Accordingly, airlines are gradually rebuilding their networks by adding frequencies and restoring service to cities that were suspended during the height of the pandemic in their respective regions.

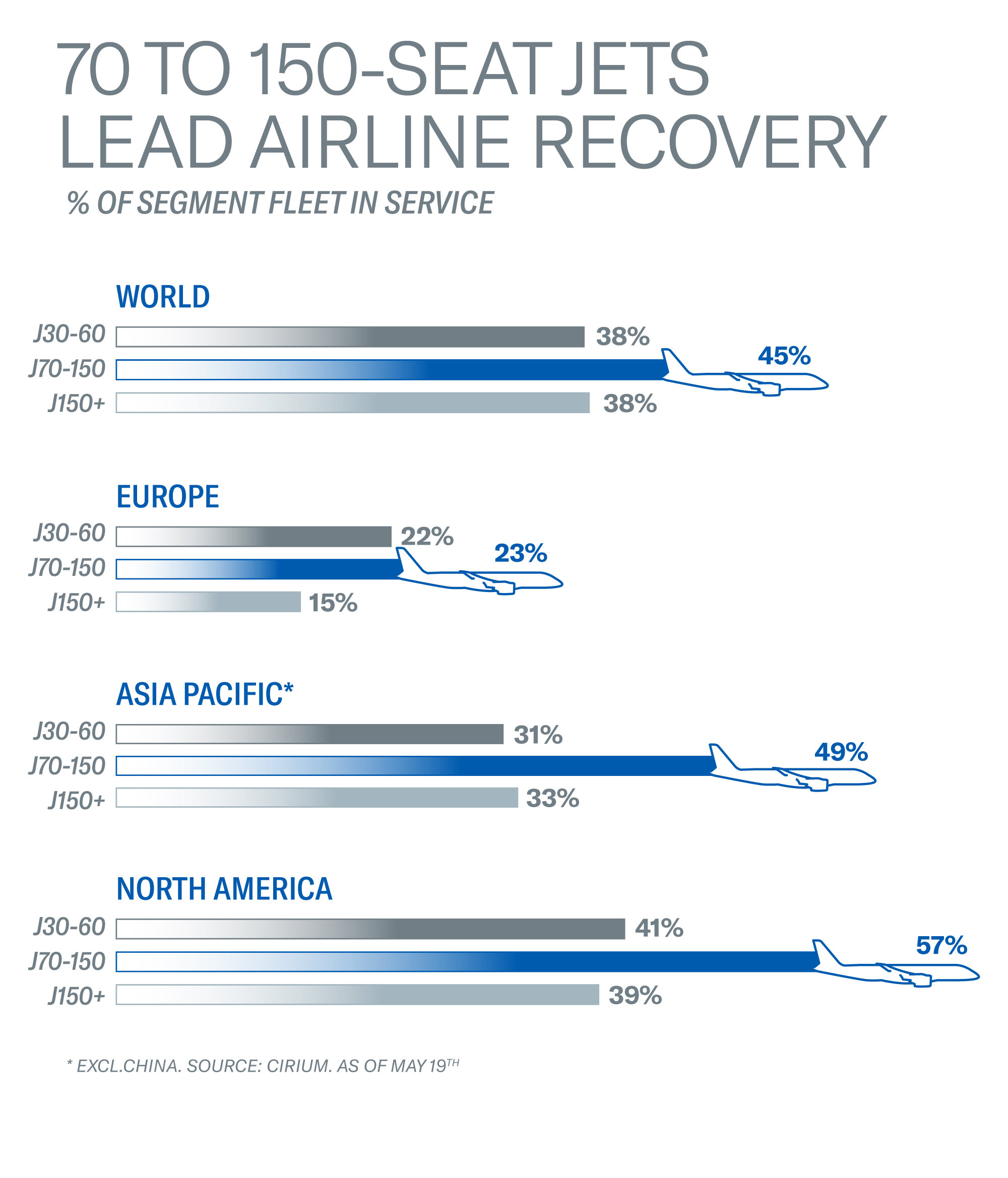

Cirium, a travel industry data and analytics company, just published statistics that show a greater proportion of the 30 to 150-seat fleet flying compared to larger jets.

These airplanes are the ideal size during this period of weak demand – they offer the right capacity and right frequency to maximize load factors and bottom-line contribution so airlines can maintain service across their networks.

According to Cirium:

- . 35% of the global commercial fleet was in service during the worst weeks of the pandemic

- . as of May 19, 2020, 41% of the world fleet was flying, a slight uptick

- . globally, the share of the 70 to 150-seat jet fleet in service is the highest (45% vs. 38% for larger narrowbodies)

Here are the details for the key world markets – Europe, the USA, and Asia/Pacific – where the infection curve is sloping down:

Deployment of small-capacity aircraft is more advantageous since demand for domestic and short-haul flights is currently greater than for long-haul international travel, where many countries still have entry restrictions for foreign passengers.

The term “right-sized” has never been more appropriate. There is still a long way to go before we can claim victory over the crises but, as the headwinds ease, airlines with right-sized aircraft will recover faster and stronger.